Bolivia has a high energy potential, both for traditional and alternative energy.

Given its geological nature, the country produces more natural gas than oil (62% of total liquids produced from condensed).

Its natural gas reserves are the second largest in South America (after Venezuela), but considering those that are liquids free, they are the first. Besides, it is expected that they will increase by 200 to 300 trillion cubic feet.

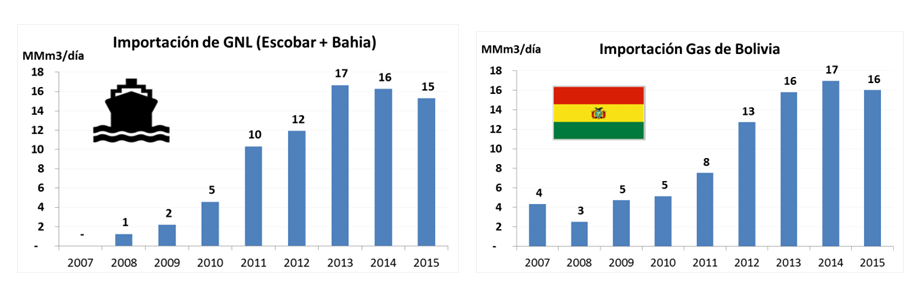

This is the basis for the Bolivian economy. The country has export contracts with the countries that surround it. For example, Brazil has a contract for 30 million cubic feet per day for 20 years.

The power sector accounts for 63% of natural gas sales.

The electricity generated in Bolivia comes from hydroelectric plants (35%) and thermal power stations (65%).

The National Interconnected System (SIN) is 90% composed by the main centers of production and consumption (La Paz, Cochabamba, Oruro, Potosi, Chuquisaca, Beni and Santa Cruz) and by isolated systems in smaller cities and towns that complete the remaining 10% of the national electricity market (Department of Pando).

Bolivia is determined to change its energy matrix, which currently is based on thermal generation.

Authorities have repeatedly pointed that their goal is to achieve a mix of 70% of power generation by hydroelectric or from alternative sources such as wind and solar, and limit thermal to the remaining 30%.

Therefore it targets to incorporate around 183 MW of renewable energy by 2025.

Two thirds of Bolivia, whose latitudinal position is between the parallels 9º 40′ S and 22º 53′ W, are situated within the range of greater solar radiation.

Thanks to this situation, the country has one of the highest levels of solar intensity in the region.

Solar incidence in the country reaches an annual average of 5,4 kWh / m² per day of intensity and 7 h/day of effective insolation.

However, perhaps because of the high availability of natural gas, Bolivia currently has no regulations and legislation that fosters sustainable development for solar installations.